Archive

Managing supply risks of rare earths

By Ruggero Golini, Filippo Valoncini, Jury Gualandris

Since the Nineties, rare earths have gained an important role in the World technological development because of their use in the so called green technologies (check our previous posts here and here).

Despite their name, these elements are not so rare; indeed, they are about 200 times more available than gold. Nevertheless, there are only few places on earth where the extraction with today’s technologies is profitable.

In the last decade, China became the monopolist in the sector of rare earth by extracting about 95% of the World total production. In the last years, with the rapid development emerging country economies, the global demand of rare earths rose dramatically bringing to an incredible increase in prices (some elements between 300% and 4000%). Many of the processing stages of the value chain are located in China. China produces more than the 95% of the rare earth oxides, about 90% of the alloys and 75% of Neodymium magnets. Furthermore, many Chinese companies develop high technology products exploiting these materials. Furthermore, the Chinese government has defined policies in terms of export quotas, incentives, customs and external investments. As a consequence of these policies, in the 2005-2009 period exports decreased by 20% down to 50,000 tons. Until 2015 they could be reduced to 35,000 tons.

Because of that, some issue in the global supply chain has emerged.

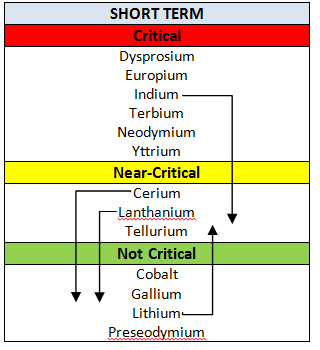

In 2011, the US Department of Energy (DOE) identified the level of criticality of the most common rare earths in the short and long term. The list shown in the figure represents the short term situation, while arrows describe how the situation will change in the future. The rank is derived according to supply risks (that includes: basic availability; competing technology demand; political, regulatory and social factors; codependence on other markets; producer diversity) and importance to clean energy technologies (that includes: clean energy demand, substitutability limitations….). Interestingly the two variables are quite correlated, that is, the most important materials are at the same time subject to higher supply risks.

Short and medium term the level of criticality of the most common rare earths

(adapted from US Department of Energy, 2011)

As we can see from the table, the situation is not going to get significantly better in the future and companies should therefore develop specific risk management strategies.

For instance, as reported by the US Department of Energy (DOE) report, Toyota followed two strategies. First of all, it tried to secure its supply of rare earths (used for hybrid and electric vehicles) by establishing a task force to monitor the risks and partnerships with few selected suppliers. Moreover, Toyota is trying to reduce the dependency on rare earths by redesigning the products, for instance, electric motors.

Sources

http://www.greenreport.it/_new/index.php?page=default&id=14067

Rare Earth Elements: The Global Supply Chain, Marc Humphries September 30, 2010

Study on Rare Earths and Their Recycling, Final Report for The Greens/EFA Group in the European Parliament, Oko Institut e.V., January 2011

Critical Materials Strategy, U.S. DEPARTMENT OF ENERGY, December 2011

Sustainability Management and Risk Management in the consumer electronics industry

by Ruggero Golini, Greta Facoetti, Jury Gualandris

This post raises and briefly addresses the following questions: can companies in the consumer electronics industry benefit from the integration of sustainability and risk management in their supply chains?

The consumer electronic industry has a highly innovative rate, provides a wide range of devices and equipment and its global value chain is very complex. In the time of one generation, the high-tech revolution has spread worldwide, with tremendous impacts on the environment and society.

In the recent years, several scandals have hit some of the industry’s leading companies, such as Apple, because of issues occurred in their supply chains.

However, despite the increasing concerns, the heterogeneity of social and environmental regulations and policies around the world is working as a barrier to the development of more sustainable supply chains. In this context, developing countries are particularly vulnerable because they perform most of the assembly operations, but they retain a low share of the value added and there is little visibility on the final markets of what happens there. Moreover, governments in question are often focused on industrial growth at the expense of environmental and social aspects.

Because of that, leading firms are trying to address environmental and social issues at different stages of their supply chain.

In our analysis, we wanted to check whether the effort put by these companies to solve an issue is related to the risks potentially occurring because of that issue.

First of all, according to the Greenpeace sustainability ranking, we have identified a set of practices electronics companies can undertake to address sustainability issues along their supply chains. Next, we have selected a cluster composed by the 10 most profitable companies in the industry (Samsung, HP, Sony, LG, Toshiba, Nokia, Panasonic, Apple, Dell and Acer). After that, we have associated a score from 0 (low level of action) to 3 (high level of action) to each company for each one of the considered practices on the basis of the same Greenpeace report. Finally, we have calculated the average level of effort for each practice in the electronic industry (Figure 1).

Figure 1 – Average level of effort put into different sustainability practices by top 10 lead firms in the electronic industry

Interestingly, energy efficiency of products is the practice that receives most effort. On the other hand, the policies on clean energy, recycling and recovery of plastic products seem to be least developed.

Next, we have calculated the risks for the leading companies associated to each issue previously identified. The global risk level, measured on a scale from 0 (no risk ongoing) to 3 (highly relevant risk), is built on considerations that concern:

- environmental risks (pollution, relaxation / lack environmental standards)

- social risks (workers’ exploitation, workers’ rights, health and life)

-

risks of supply (shortage, supply disruption, conflict zones)

The scores were given on the basis of information got from multiple sources (the complete list is indicated in the references.

Finally, a comparison between “level of effort” and the “level of risk” for each specific environmental issue has been performed (Figure 2). This analysis allows to reconnect potential sustainability risks with what the companies are actually doing.

Figure 2 – Comparison between the level of effort and the level of risk

The resulting picture shows that for the energy efficiency issues (the first 5) the level of effort matches the risk. However, the other risks, especially the last four related to the supply chain are associated to the highest level of risk but the effort is not apportioned.

This result can be dependent on the fact that working on the supply chain is more difficult than other areas. However, another reason could be that the effort of the companies is driven by the pressures of the stakeholders rather than by a critical analysis of the issues in the global value chain.

References

- “Carbon EmissionsMeasuring the risk. An S&P 500 NFS International Sector Report” authored by Trucost

- “Sustainable Water Management for Electronics Industry”, authored by Siemens

“Green Management Activities and Performance” authored by Samsung, Electronics Sustainability Report 2012 - “Responding to Climate Change Risk: Basic of GHG Emission Inventories”, authored by E Source Companies LLC 2006

- “Managing Supply Chain GHG Emissions, lesson learned for the road ahead”, authored by EPA, 2010

“COOL IT, Leaderboar December 2010”, authored by Greenpeace - “The Hidden Consequences, The cost of industrial water pollution on people, planet and profit”, authored by Greenpeace

- “Effective action on global warming prevention by the electrical and electronics industries” authored by Liason Japanese Group

- “Water Scarcity &Climate Change: Growing risk for business & investors”, authored by The Pacific Institute, 2009

- ” Conflict minerals: What you need to know about the new disclosure and reporting requirements and how Ernst & Young can help”by Ernst&Young

- “I costi umani di un Ipad”, authored by Internazionale n°934, February 2012

- “Il disastro giapponese mette a rischio la fornitura di batterie e memorie cellulari”, Il Sole 24 Ore, 14 March 2011

- “Building Resilience in Supply Chains”, authored by Accenture World Economics Forum, 2013

” Sustanaibility: A risk Management perspective”, authored by David Singleton www.sustdev.org SDI 1616/5 - ” The case for integrating sustainability and risk management: why sustainability must be a priority for corporate risk managers”, authored by Aon Corporation, 2009

- “Knowing your risk: managing the value at risk from sustainability issues”, authored by PWC

eventuali report aziendali

Similar products, different footprint stories

by Ruggero Golini and Marco Gervasoni, Università degli Studi di Bergamo

In a world of global supply chains, two products that look very similar, can have very different footprint stories.

The Life Cycle Assessment analysis applied to the environmental footprint of the products along the supply chain offers an interesting perspective on how products that look similar can be, in practice, very different. This particularly true in global supply chains where the technological choices are combined with localization and transportation choices.

Because of that, we compared the carbon footprint of two pairs of sunglasses (Ray-Ban RB3025 Aviator and Oakley Whisker) made by the same company (Luxottica) and using information from the EPD (Environmental Product Declaration) developed by the International EPD. We also used Sourcemap to draw maps of the supply chains of these two products.

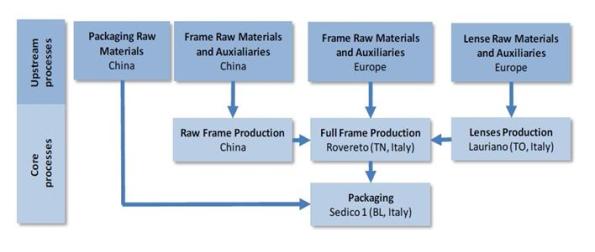

The first sunglasses are the Ray-Ban RB3025 Aviator. The supply chain is quite straightforward with raw materials and components (upstream processes) coming from China and Europe. Then part of the manufacturing activities (core processes) is performed in China (for the frame) and the rest in Italy.

From the geographical point of view, the supply chain appears as follows (the locations are approximated). (https://sourcemap.com/view/5390#):

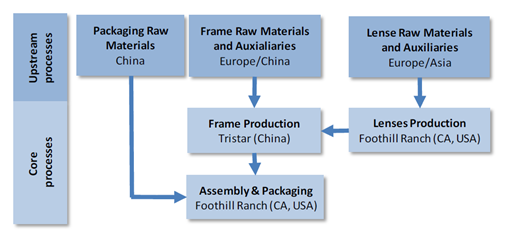

On the other side, the supply chain of the Oakley Whiskers involves less partners, but more countries. In fact, part of the production (the lenses) is made in California (USA) and sent to China.

The resulting map, looks like this (https://sourcemap.com/view/5406#):

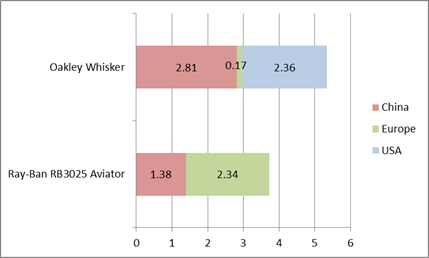

Focusing on the CO2 emissions, we can notice that the Oakley Whisker produce 13% more CO2, mainly because of production processes.

CO2 emissions (in Kilograms) – source: authors elaboration. The emissions due to transportation are based on authors0 estimates and checked with SourceMap statistics

However, it is worth noticing that the Oakley have about half of the weight of the Rayban (65 g vs 121 g), mainly because of the glass-made lenses of the latter. This means that, because of a more complex supply chain and production process, the Oakley have almost double CO2 emissions per gram.

Total KgCO2 / gram

Moreover, because of supply chain localization choices the distribution of CO2 emission is quite uneven among countries. The next figure reports the emissions of CO2 in the different countries (excludes transportation):

KgCO2 emissions by country

In conclusion, we can see how supply chain choices can strongly affect CO2 emission and where these emissions are produced and how each product has it is own story.

Now, can we help you in tracking your footprint along your supply chain? Let us know!

References

For Ray-Ban RB3025 Aviator: http://gryphon.environdec.com/data/files/6/8960/epde405_Ray-Ban_%20Aviator%203025.pdf

For Oakley Whisker: http://gryphon.environdec.com/data/files/6/8964/epde409_Oakley_Whisker.pdf

The copper global value chain and the black hole of China

Raw materials global value chains are becoming increasingly relevant for the world economy. In this article, we focus on the global value chain of copper and copper-based alloys that are used in a broad variety of applications in everyday life. Copper, in fact, is an indispensable asset today and presumably will continue to be so in the future. However, its global value chain shows some peculiar characteristics with a dominant role of very few countries.

The copper global value chain can be divided into four main stages:

- mining production

- fabrication and manufacture

- product use

- end-of-life management

Let’s focus on the first two stages (mining production and fabrication).

The mining production phase includes the following sub-phases: extraction, smelter and refinery.

Extraction of copper-bearing ores is the initial production activity. There are three basic ways to mine copper: surface, underground mining and leaching. Open-pit mining is the predominant mining method in the world. In the beginning of the 20th century world production was less than 500 thousand tons of copper, but then it has grown about by 3% per year to reach over 16 million tons in 2011. The leading country is South America that grew from less than 750 thousand tons of copper in 1960 to 7 million tons in 2011 (of which 5.3 come from Chile).

Next, smelting is the process used to produce pure copper. The output of this phase is called anode or blister. In 2011, world copper smelter production reached 15.8 million tons copper (that is, about 100% of the extracted copper). Recently, the new process of leaching has been introduced and increasingly used (SX-EW). Primary smelters use mine concentrates as their main input. Secondary copper smelters use copper scrap that derives from either metals discarded in fabrication or finished product manufacturing processes (“new scrap”) or obsolete end-of-life products (“old scrap”). In this sub-phase Asia is the dominant player with a share of world copper smelter production jumped from 27% in 1990 to 55% in 2011. Taking into account 2011 primary and secondary smelting, China accounted for around 30% of world copper smelter production, followed by Japan (9%), Chile (9%) and the Russian Federation (5%). Finally, the copper is refined.

After that, in the fabrication phase we analyze the production of semis. The semis is the copper with a defined shape such as cathodes, wire bar, ingot, billet slab and cake into semi-finished copper and copper alloy products. Semis fabricators are considered to be the “first users” of refined copper and include ingot makers, master alloy plants, wire rod plants, brass mills, alloy wire mills, foundries and foil mills. Also in this phase, Asia is the dominant player and in fact it accounted for 66% of semis production in 2010 with more than 15.2 million metric tons, up from 22% in 1980.

From this brief analysis the most relevant result is the leading role of China. While Chile is the main exporter of copper, China has the lead in the following phases (table 1). This explains why there is a huge export flow from Chile to China or raw copper, but then the international trade flows of refined copper are very limited especially those out flowing from China. As a matter of fact, the production remains concentrated in China until the copper is used in final products creating a kind of black hole.

Table 1 Ranking dominant countries involved in copper production.

References:

-

International Copper Study Group, ICSG World Copper Factbook 2012, http://www.icsg.org/

-

Copper Development Association Inc., Annual Data 2012: Copper Supply & Consumption 1991–2011, http://www.copper.org/resources/market_data/pdfs/annual_data.pdf

-

MBendi Information Services, http://www.mbendi.com/indy/ming/cppr/p0005.htm

Global Supply Chain Configurations In The Manufacturing Industry

Global supply chain management refers to exchanging information and coordinating efforts with suppliers and customers, in order to support globalization strategies determined by companies. Globalization does not only refer to the act of selling all around the world, but also to sourcing and manufacturing on the global scale, and all of this needs to be coordinated flawlessly.

Global supply chain management refers to exchanging information and coordinating efforts with suppliers and customers, in order to support globalization strategies determined by companies. Globalization does not only refer to the act of selling all around the world, but also to sourcing and manufacturing on the global scale, and all of this needs to be coordinated flawlessly.

Within this context, a recent book and an article we published (Golini, 2011; Caniato, Golini and Kalchschmidt, 2013) provides a conceptualization of the above-mentioned phenomena and ends up with the guidelines considered to be useful for companies in supporting their globalization strategies. First of all, four different global supply chain configurations are identified. Next, for each configuration, the best investments in the supply chain that aim to improve performance are defined. Finally, the effect of contextual variables is taken into account, and, in particular, it shows that the structure of the supply chain from one end to another (also called the value chain) holds a crucial role. The results are supported by empirical data from an international survey (International Manufacturing Strategy Survey).

The four global supply chain configurations identified

Four main configurations of global supply chain according to the percentage of sourcing, manufacturing and sales outside the continent are identified (See Figure). These configurations have been labeled and defined as follows:

- Locals: local sourcing, manufacturing and distribution;

- Barons: local sourcing and manufacturing, global distribution;

- Shoppers: global sourcing, local manufacturing and distribution;

- Globals: global sourcing, manufacturing and distribution.

Next, we considered the investments made to manage effectively the supply chain. This investments are classified in:

- Sourcing-related investments, that are coordination of the flows of goods and information with suppliers, suppliers development, specific supply strategies and risk management;

- Distribution-related investments, that are coordination of the flows of goods and information with customers and specific distribution strategies.

Locals, as a general tendency, invest less than the others; specifically, Locals invest less than Shoppers on supplier development and distribution strategy; Locals invest less than Barons in coordination with suppliers; Locals invest less than Globals in supplier development.

Finally, looking at the performance (cost, quality, delivery, lead time, flexibility), we found that every cluster can benefit from investment in the supply chain, usually in more than one performance indicator. However, looking at each cluster we found more detailed results. In particular,:

- Locals can further improve their delivery, lead time and quality performance if they review their distribution strategy and implement supplier development;

- Barons, on the contrary, should be careful about investment in coordination with suppliers and customers, as this appears to be detrimental for their quality performance;

- Shoppers benefit from every supply chain investments, without specific areas that are more or less beneficial;

- Globals receive very little help from investments in the supply chain, as their effect is limited to improve flexibility performance. Probably, this can depend on the many different sub-configurations that Globals can have and that make investment in the supply chain more or less beneficial.

This work offers a new perspective on global supply chain management useful for research and practice. Results provide evidence of the different configurations of globalization that can and are adopted by firms, providing some hints on the characteristics of each of them, which can help managers to define their globalization strategy. Moreover, this research shows which investments in the supply chain are more beneficial to improve the performance according to the different configurations.

References

Golini, R., 2011. Global Supply Chain Management In The Manufacturing Industry: Configurations, improvement programs and performance. Sestante – Bergamo University Press, Bergamo.

Performing an effective global sourcing: supplier selection criteria and investments in the supply chain

by Ruggero Golini and Luca Savoldelli – Università degli Studi di Bergamo

Global souring is often seen as a way to reduce costs, but when considering all the implied costs (for instance, taxes, transportation, insurances, etc.) the costs can become even higher. To analyze how to keep these costs down, we classified companies in the following way:

The green group represents locals who purchase mainly within their region, the blue group identifies those performing global sourcing from around the World with higher procurement costs and, finally, the red group represents global enterprises that source in the world but with competitive procurement costs. Of the 585 plant considered within the IMSS V database (www.manufacturingstrategy.net), 302 are green, 101 are blue and only 48 are red.

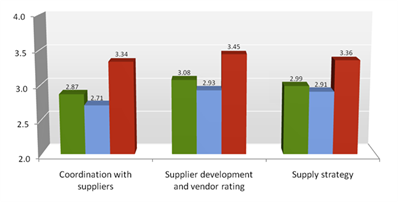

So what do red companies different? We compared their criteria of selection of suppliers and the investments made in the supply chain.

The selection criteria are very similar among the groups: the most important factors are: quality of product / service and delivery performance (that is, delivery speed and reliability). Lowest price comes third also for global sourcing companies. Interestingly, the main difference between the red group and the others are on the less important factors: logistical costs, innovation and co-design and availability to share information.

Figure 1 – Supplier selection criteria (importance measured from 1 to 5)

When looking at the investment in the supply chain the difference between the red group and the others is much clearer. Companies performing global sourcing competitively, do invest more in coordination with suppliers, supplier development and vendor rating and in reviewing their supply strategy for instance, through supply base consolidation.

- Figure 2 – Investment in the supply chain in the last 3 years (measured from 1 to 5)

In conclusion, the companies in the red square , that are those performing global sourcing at lower costs, seem to adopt a collaborative approach with their suppliers. These companies select few suppliers on their willingness to establish long-term relationships and then they invest a lot in sharing information and take joint decisions.

However, the literature reports several risks in this strategy that should be carefully considered. First, when sharing information, there is the risk of information spill-over and suppliers can even become competitors. Next, in emerging markets there are constantly new suppliers available, so it is important to continue scouting the market seeking for the best opportunities and be ready to switch supplier. In our sample, for instance, red companies are also those that use significantly electronic instruments to scout new suppliers. Finally, large global suppliers require high volumes and many orders so bind them with long term contracts con be difficult and not viable to smaller companies.

The role of strategic reasons for offshoring and nearshoring success

by Federico Caniato (Politecnico di Milano), Ruggero Golini and Matteo Kalchschmidt

by Federico Caniato (Politecnico di Milano), Ruggero Golini and Matteo Kalchschmidt

When investing across borders, companies may incur in several problems not experienced at the domestic level and these problems can change from country to country (World Bank Group, 2010). Moreover, managing a global manufacturing network can pose some issues to the profitability of the company: because of that, in past years, many companies backshored the production home (Kinkel & Maloca, 2009).

One of the key aspect, even if under investigated, is the strategic reason why the company moved the production abroad.

To analyze the problem, we used data collected in 2009 within the fifth edition of the International Manufacturing Strategy Survey (IMSS 5). We selected only Western European companies, and, in particular, 227 companies provided information for this research. Companies are mainly small sized (47.6% of the sample) but also medium and large companies are represented. Different industrial sectors from the assembly industry are considered, mainly from the manufacturing of fabricated metal products, machinery and equipment.

The problem is that for European countries literature does not provide much evidence about the differences in the strategic reasons between offshoring (defined as moving the production outside Europe) and nearshoring (defined as moving the production to another country within Europe).

Our data show that for both nearshoring and offshoring the cost driver (that is, seek for lower input and work cost) is the most important. Then, for nearshoring, the entrepreneurial driver (that is, seek for new markets, establish new business relationships, follow customers, react to competitors…) see and resource driver (that is, seeking for new technologies and skills) follow, sharing the second place. On the contrary, for offshoring, the entrepreneurial driver follow and resource driver comes last (Table 1).

Table 1 – Comparison of the reasons for offshoring and nearshoring (1-5 scale)

|

Nearshoring |

Offshoring |

|||

|

|

Mean |

Rank |

Mean |

Rank |

| Cost driver (seek for lower operational costs) |

2.7 |

1 |

2.7 |

1 |

| Entrepreneurial driver (seek for new markets, establish new business relationships, follow customers, react to competitors…) |

2.1 |

2 |

2.2 |

2 |

| Resource driver (seeking for new technologies and skills) |

2.2 |

2 |

1.9 |

3 |

Next we looked at the performance obtained measured as the Return Of Investment in the last three years:

Next we looked at the performance obtained measured as the Return Of Investment in the last three years:

- For nearshoring the entrepreneurial driver is significant in explaining a higher performance

- For offshoring, the resource driver, despite its lower importance (Table 1), has a strong positive and significant impact on the performance.

In conclusion, we did not find any significant difference in business performance among companies that offshored or nearshored. This highlights that is not where the companies invest that matters, but how. In particular, companies should look at moving the production abroad as a mean to conquer new markets (entreprenurial driver) or find new skills and resources, rather than a way to reduce costs.

From: Caniato, F., Golini, R., Kalchschmidt, M., 2011. Offshoring and nearshoring success: the importance of strategic reasons, 18th EurOMA Conference, Cambridge (UK). Downlaod paper: EurOMA2011_0175

References

Buckley, P. J., & Casson, M. (1976). The future of the multinational enterprise. London: Macmillan

Dunning, J. H. (1998). Location and the multinational enterprise: A neglected factor. Journal of International Business Studies, 29(1), 45-66.

Kinkel, S., & Maloca, S. (2009). Drivers and antecedents of manufacturing offshoring and backshoring–A German perspective. Journal of Purchasing and Supply Management, 15(3), 154-165.

Roza, M., Van den Bosch, F. A. J., & Volberda, H. W. (2011). Offshoring strategy: Motives, functions, locations, and governance modes of small, medium-sized and large firms. International Business Review.

Sakthivel, S. (2007). Managing risk in offshore systems development. Communications of the ACM, 50(4), 69-75.

World Bank Group. (2010). Investing Accross Borders.

Vendor Managed Inventory for Global Sourcing Companies

By Ruggero Golini and Martina Lozza, Università degli Studi di Bergamo

By Ruggero Golini and Martina Lozza, Università degli Studi di BergamoVendor Managed Inventory (VMI) is an operating model in which the supplier delivers its good to the customer but the actual sale is postponed after the actual use/sale by the customer. The supplier, which can be a manufacturer, reseller or a distributor monitors the customer’s inventory levels and makes inventory replenishment decisions regarding order quantities, shipping and timing.

The advantages of implementing VMI program can be summarized as: reduced inventory costs, better response to market changes, reduction in demand uncertainty and more flexibility in production planning and distribution.

Recentely, we focused on how VMI can support global sourcing.

As we know, there are several reasons for adopting global sourcing such as lower prices, quality technology access, access to new markets, shorter product development and life cycles, comparative advantage. However, the adoption of global sourcing often leads to some problems such as increase of inventory level because of the average inventory level depends on the supply lead time and variability, which get higher when the distance between supplier and buyer increases.

According to our analysis, the implementation of VMI can be a very effective way to reduce the inventory level for global sourcing companies.

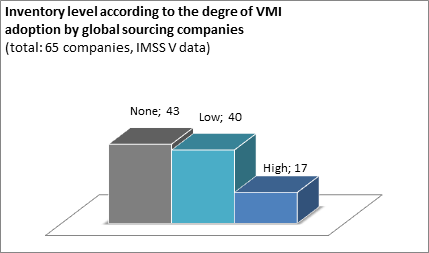

We used the fifth edition of the International Manufacturing Strategy Survey (www.manufacturingstrategy.net) and we picked the companies with a relevant adoption of global sourcing (more than 30% of their purchases comes from outside the continent). We can see that 75% of the companies uses VMI with suppliers but only 26% declare to have a high and spread adoption.

The next histogram shows the average level of inventory (measured in days of production carried in the material and components inventory) and it is evident that when the VMI is highly implemented the inventory level decreases significantly.

Obviously implementing VMI when suppliers are far away can be difficult due to geographical and linguistic distance and the necessary conditions have to be met. However the positive impact VMI is remarkable and, especially when holding inventories is costly (like in these days), global sourcing companies should definitely consider VMI into their supply chain investments portfolio.

Bibliography

Danese, P. 2006. The extended VMI for coordinating the whole supply network. Journal of Manufacturing Technology Management 17 (7), 888–907.

Disney, S.M., Towill, D.R. 2003. The effect of vendor managed inventory (VMI) dynamics on Bullwhip Effect in supply chains. International Journal of Production Economics, Volume 85, Issue 2, pp. 199-215.

Golini, R., Kalchschmidt, M., 2011. Moderating the impact of global sourcing on inventories through supply chain management. International Journal of Production Economics, 133, 86-94.

The reaction of supply chains to the crisis: the shifts of global trade flows

As a reaction to the global crisis, supply chains are changing their geography. The traditional western markets are not recovering from the crisis and seems that their economies are following a W or L-shape pattern rather than the expected V-shape. Because of that, global supply chains are shifting to other markets, and the so called South-South trades are increasing. If we look at the table (2010 WTO data of merchandise trade), we can see that the higher flows still occur from Asia to Europe and North America (about 1.6 trillion dollars) and vice versa (about 800 billion dollars). China accounts two thirds of these flows. However, looking at the difference between 2008 and 2010 (only two years) we can see that the flows from Asia to Europe and North America have been quite stable. All the other flows directed to North America and Europe have decreased more than 5% (for instance from South and Central America or Africa). On the other side, all the flows directed to Asia increased more than 5%, except from Middle East that has intensified the exchanges with South and Central America. Also the exchanges from Asia to South and Central America and to Africa have increased more than 5%. It will be interesting to follow the trend as soon as 2011 data will be released. So far, looks like Asia represents the new market where flows from every continent are directed. On the other side, Asia which is a huge manufacturing country is seeking for new markets (for instance South and Central America or Asia) to reduce the dependence from the uncertain traditional European and North American markets.

As a reaction to the global crisis, supply chains are changing their geography. The traditional western markets are not recovering from the crisis and seems that their economies are following a W or L-shape pattern rather than the expected V-shape. Because of that, global supply chains are shifting to other markets, and the so called South-South trades are increasing. If we look at the table (2010 WTO data of merchandise trade), we can see that the higher flows still occur from Asia to Europe and North America (about 1.6 trillion dollars) and vice versa (about 800 billion dollars). China accounts two thirds of these flows. However, looking at the difference between 2008 and 2010 (only two years) we can see that the flows from Asia to Europe and North America have been quite stable. All the other flows directed to North America and Europe have decreased more than 5% (for instance from South and Central America or Africa). On the other side, all the flows directed to Asia increased more than 5%, except from Middle East that has intensified the exchanges with South and Central America. Also the exchanges from Asia to South and Central America and to Africa have increased more than 5%. It will be interesting to follow the trend as soon as 2011 data will be released. So far, looks like Asia represents the new market where flows from every continent are directed. On the other side, Asia which is a huge manufacturing country is seeking for new markets (for instance South and Central America or Asia) to reduce the dependence from the uncertain traditional European and North American markets.

2010 merchandise trade data (WTO) – The darker the color, the greater the flow

Global CO2 emissions in the last 150 years

In the last decades, much attention has been given to global warming and the need for CO2 emissions reduction by society and companies.

In the last decades, much attention has been given to global warming and the need for CO2 emissions reduction by society and companies.

This is related and affects also the way in which global supply chains are managed. For instance, lead firms (usually located in developed countries) push suppliers (both in developed and developing countries) to adopt more environmentally friendly technologies, enabling them to reduce CO2 emissions.

In the same time, governments negotiate on targets (take, for instance, the Kyoto protocol), define new regulations and can in turn put pressure on the companies to shift to the adoption of greener technologies.

When discussing these topics, however, we often miss the big picture. What does the long term trend look like? What has actually been done by developed and developing economies? Gapminder (www.gapminder.org ) has developed a nice tool for representation of World Bank data (including CO2 emission) that can help us.

So, let’s create a graph where every dot represents a country. The size of the dot represents the total CO2 emissions. Basically, CO2 emissions depend on the number of people (horizontal axis) and the CO2 emissions per person (vertical axis – a measure of individual consumption). Finally, let’s focus on four countries: Germany, Untied States, India and China, and observe the evolution from 1860 to 2008.

We can identify 5 periods:

- 1860-1900: For the first forty years we have data only for Germany and United States. They start with the same population (around 35 million). Over time, the population of the United States doubles while the CO2 emissions per person in both the United States and Germany increases of ten times in relation with the Second Industrial Revolution.

- 1900-1928: India and China appear on the picture. They already have a much larger and faster growing population with very low and stable emissions per capita. In this period, the First World War takes place, but the effect on the emissions of Germany and United States is limited. Interestingly enough, the United States are able to further increase their consumption (that is, emissions) faster than Germany.

- 1929-1960: the Great Depression in 1929 causes a significant decrease in the United States’ emissions, while the Second World War causes a huge decrease of German emissions. In India and China, the population continues to grow but not the emissions per capita.

- 1960-1990: Germany and the United States recover fast from the crises and maintain a relatively stable situation in terms of emissions (that is, consumptions) and population. In India and China, the population continues to increase with limited increase in the emissions.

- 1990-2008: the United States remain stable, while Germany reduces its emissions per capita. In 2008, in Germany we witness about half of the Americans’ emissions per capita. However, these are small changes compared to those of India and China. In China, the population growth slows down, but the emissions per capita start increasing. It seems that China is now moving vertically, as Germany or the United States did in the 1860s. The problem is (look at the size of the bubble) that China is already emitting as much as the United States. India is instead still on a fast growth population route, so its vertical movement will probably arrive later.

You can also find the original plot at: www.bit.ly/xhWizC

Università degli Studi di Bergamo